회귀(Regression) - 규제

[참조] 패스트캠퍼스 - 직장인을 위한 파이썬 데이터분석 올인원 패키지 Online.

규제(Regularization)

규제란 학습이 과대적합 되는 것을 방지하고자 일종의 penalty를 부여하는 것을 말한다.

- L2 규제(L2 Regularization)

- 각 가중치 제곱의 합에 규제 강도(Regularization Strength) λ를 곱함

- λ를 크게하면 가중치 감소(규제 중시)

- λ를 작게하면 가중치 증가(규제 중시 X)

- L1 규제(L1 Regularization)

- 가중치 합에 규제 강도 λ를 곱해 오차에 더함

- 어떤 가중치(w)는 0이 되어 모델에서 제외되는 특성이 생길 수가 있음

L1 규제는 모델에서 제외되는 특성이 있어 L2 규제가 더 안정적이라 더 많이 사용된다.

릿지(Ridge)

L2 규제를 사용한 모델이 릿지 모델이다. \[Error=MSE+αw^2\]

릿지 모델 로드

from sklearn.linear_model import Ridge

규제를 위한 값

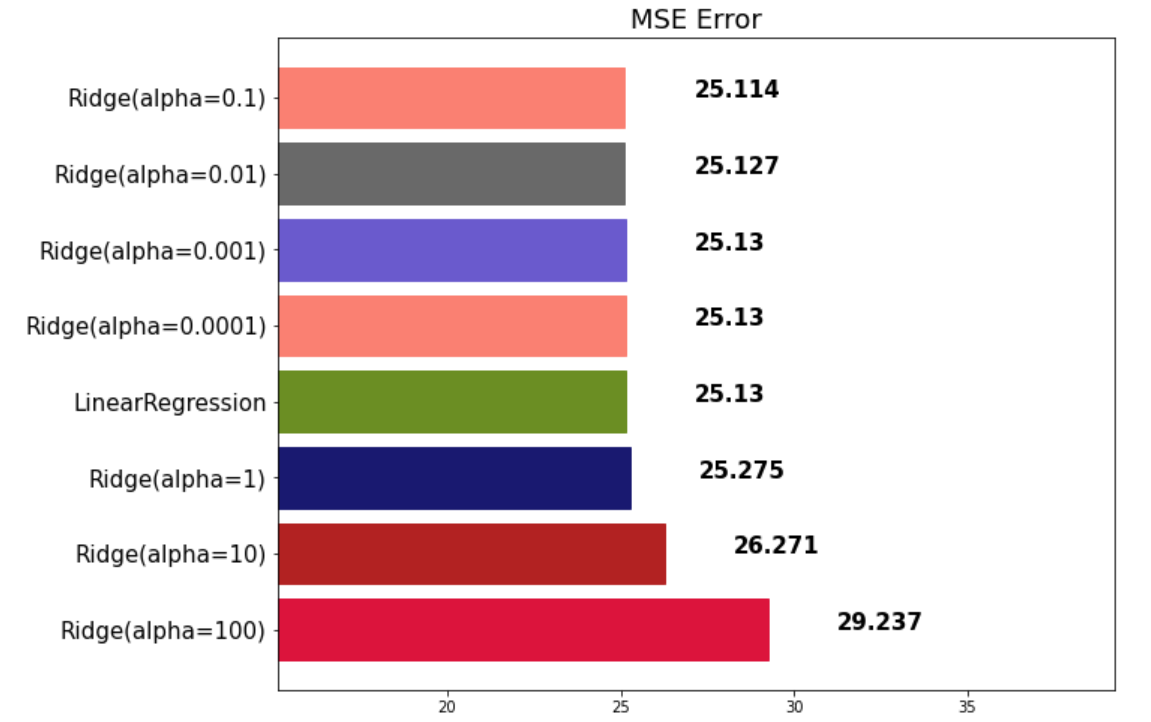

alphas = [100, 10, 1, 0.1, 0.01, 0.001, 0.0001]

- 값이 커질수록 규제가 커짐

릿지 모델 구현 및 시각화

for alpha in alphas:

ridge = Ridge(alpha=alpha)

ridge.fit(x_train, y_train)

pred = ridge.predict(x_test)

mse_eval('Ridge(alpha={})'.format(alpha), pred, y_test)

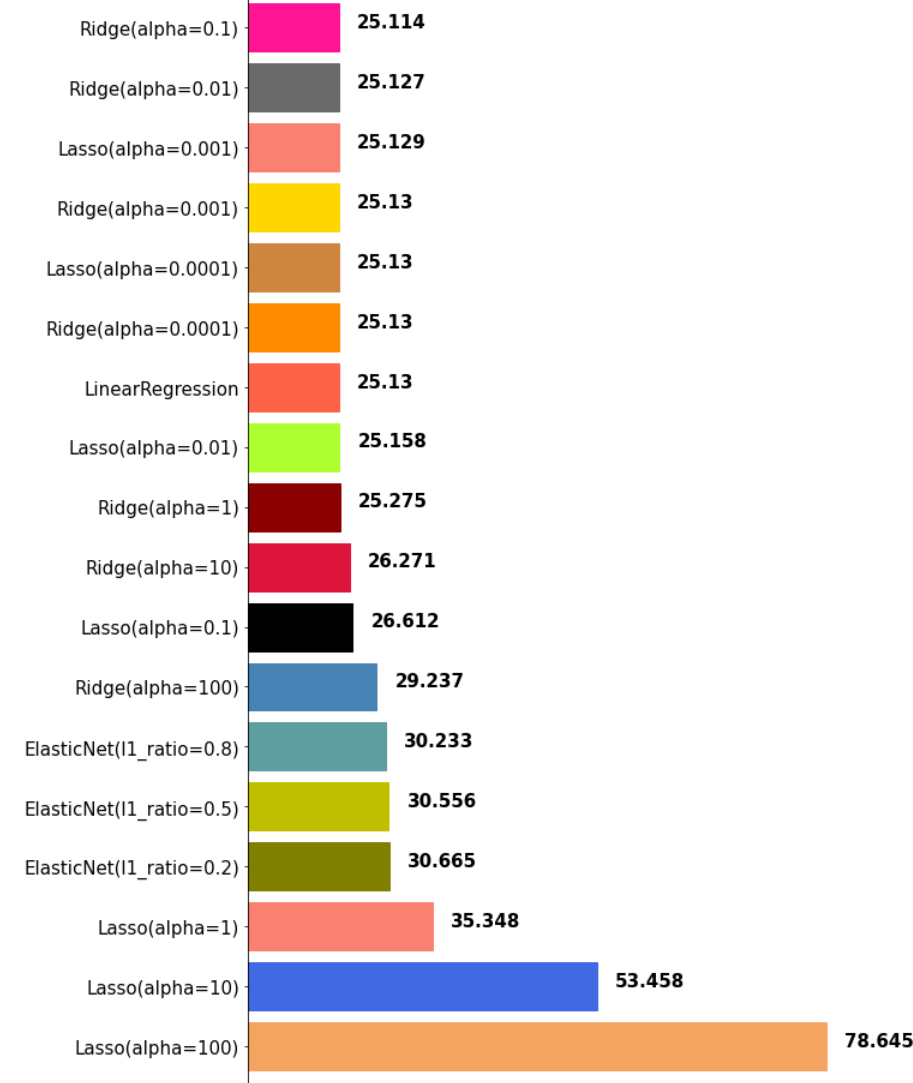

이처럼 α 값에 따른 MSE 수치를 확인할 수가 있다.

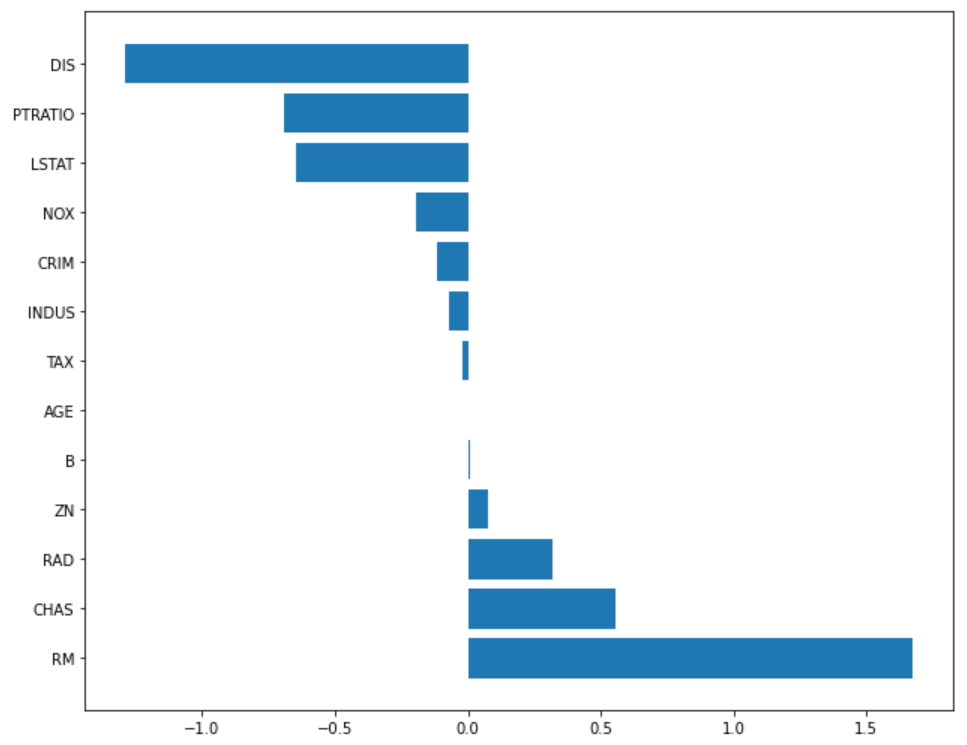

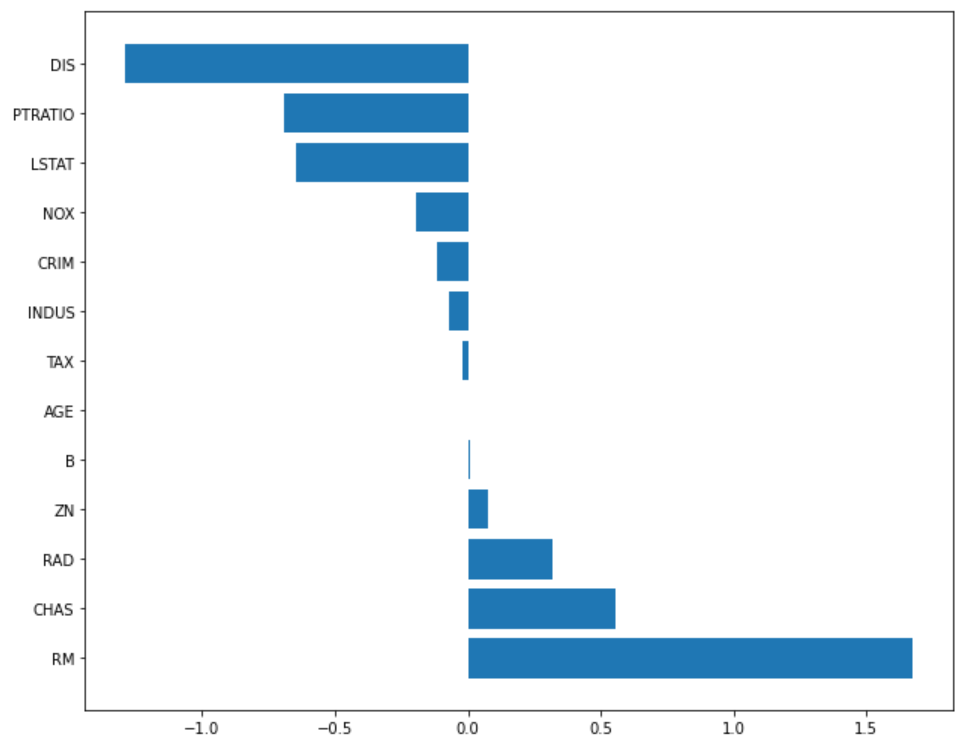

릿지 모델 가중치(coefficient) 확인

def plot_coef(columns, coef):

coef_df = pd.DataFrame(list(zip(columns, coef)))

coef_df.columns=['feature', 'coef']

coef_df = coef_df.sort_values('coef', ascending=False).reset_index(drop=True)

fig, ax = plt.subplots(figsize=(9, 7))

ax.barh(np.arange(len(coef_df)), coef_df['coef'])

idx = np.arange(len(coef_df))

ax.set_yticks(idx)

ax.set_yticklabels(coef_df['feature'])

fig.tight_layout()

plt.show()

위 함수를 이용해 α 값을 다르게 했을 때 coef를 확인해 보도록 한다.

ridge_100 = Ridge(alpha=100)

ridge_100.fit(x_train, y_train)

ridge_pred_100 = ridge_100.predict(x_test)

ridge_001 = Ridge(alpha=0.001)

ridge_001.fit(x_train, y_train)

ridge_pred_001 = ridge_001.predict(x_test)

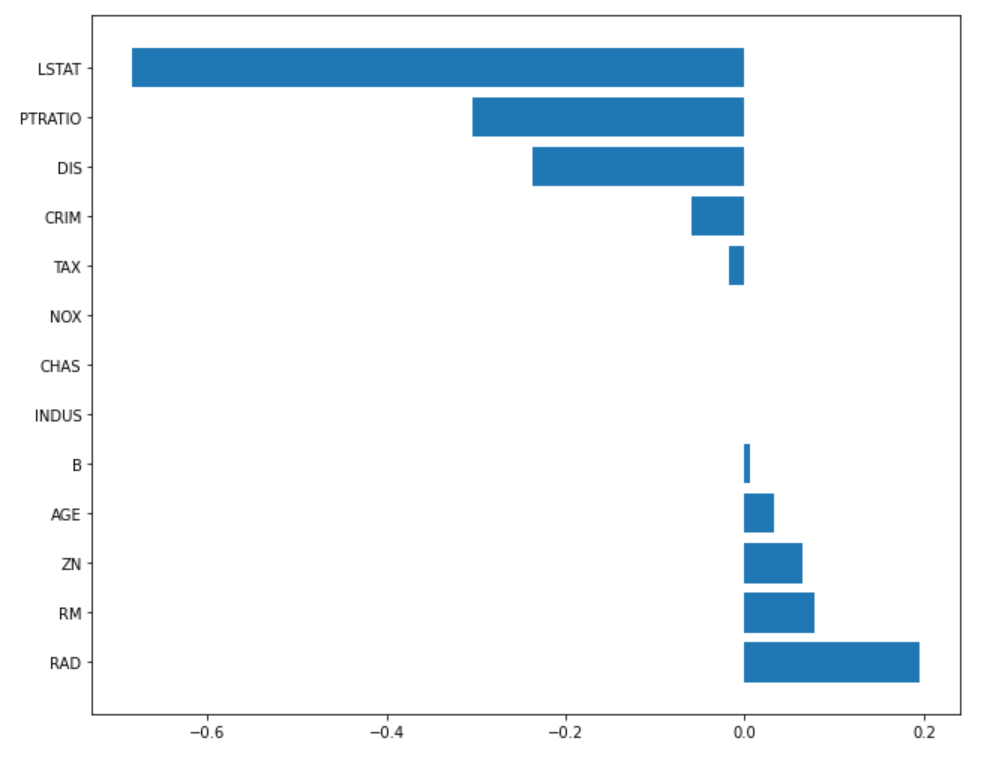

α = 100

plot_coef(x_train.columns, ridge_100.coef_)

α = 0.001

plot_coef(x_train.columns, ridge_001.coef_)

라쏘(Lasso)

L1 규제를 사용한 모델이 라쏘 모델이다. \[Error=MSE+α|w|\]

라쏘 모델 로드

from sklearn.linear_model import Lasso

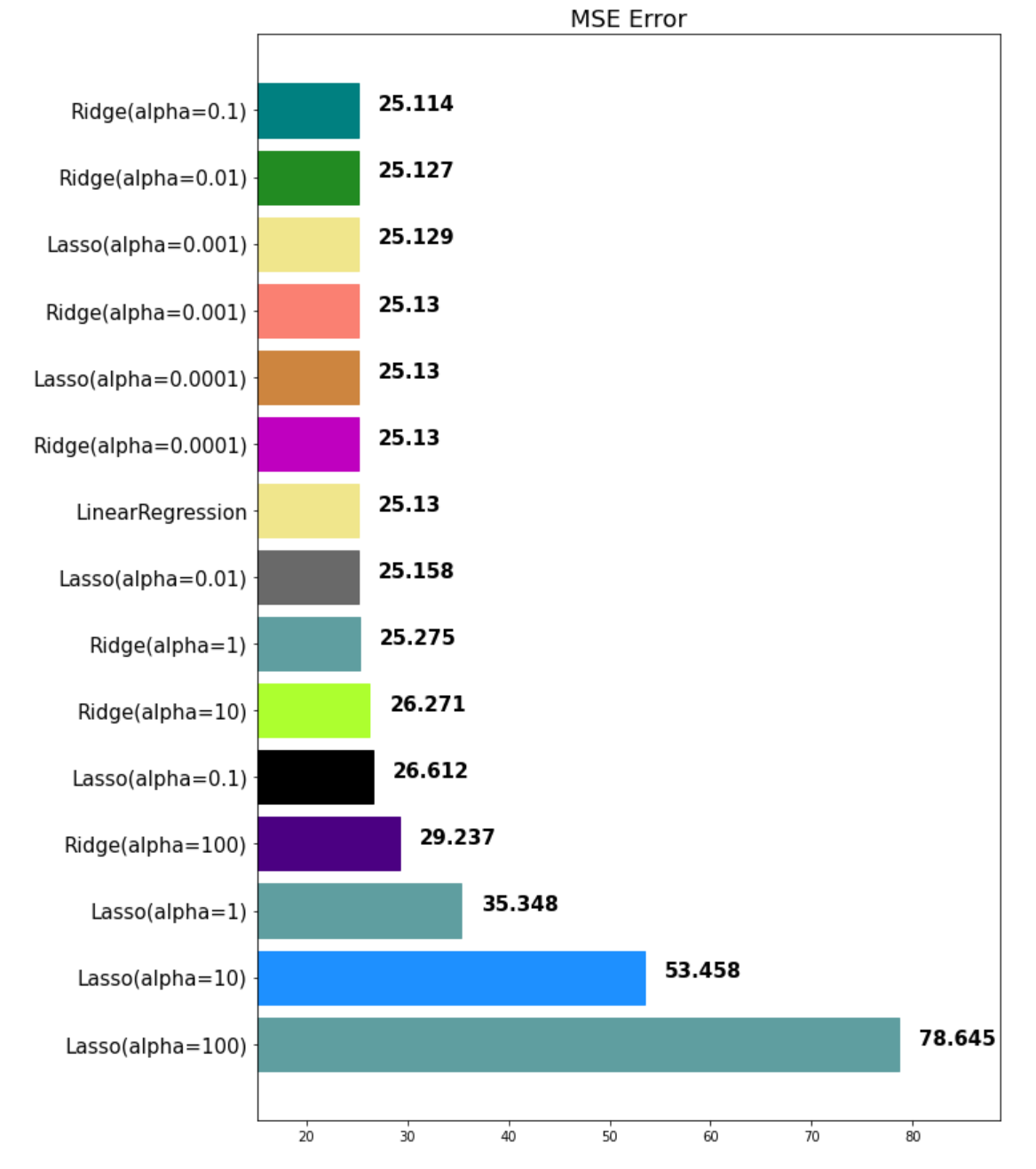

규제를 위한 값

alphas = [100, 10, 1, 0.1, 0.01, 0.001, 0.0001]

- 값이 커질수록 규제가 커짐

라쏘 모델 구현 및 시각화

for alpha in alphas:

lasso = Lasso(alpha=alpha)

lasso.fit(x_train, y_train)

pred = lasso.predict(x_test)

mse_eval('Lasso(alpha={})'.format(alpha), pred, y_test)

이처럼 α 값에 따른 MSE 수치를 확인할 수가 있다.

라쏘 모델 가중치(coefficient) 확인

위 plot_coef() 함수를 이용해 α 값을 다르게 했을 때 coef를 확인해 보도록 한다.

lasso_100 = Lasso(alpha=100)

lasso_100.fit(x_train, y_train)

lasso_pred_100 = lasso_100.predict(x_test)

lasso_001 = Lasso(alpha=0.001)

lasso_001.fit(x_train, y_train)

lasso_pred_001 = lasso_001.predict(x_test)

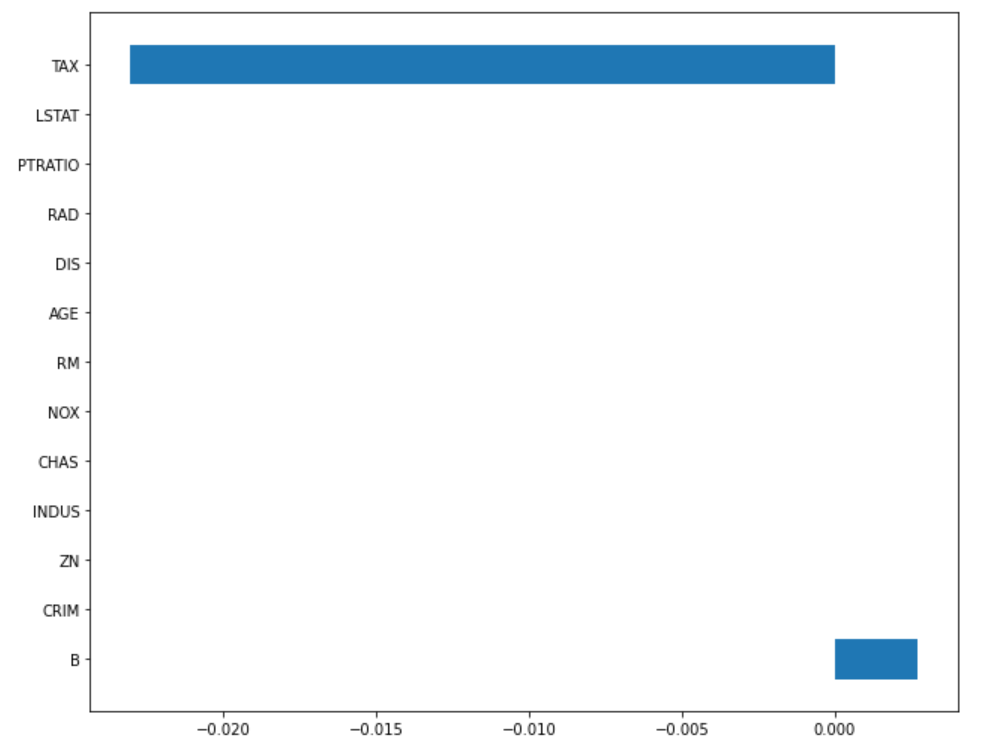

α = 100

plot_coef(x_train.columns, lasso_100.coef_)

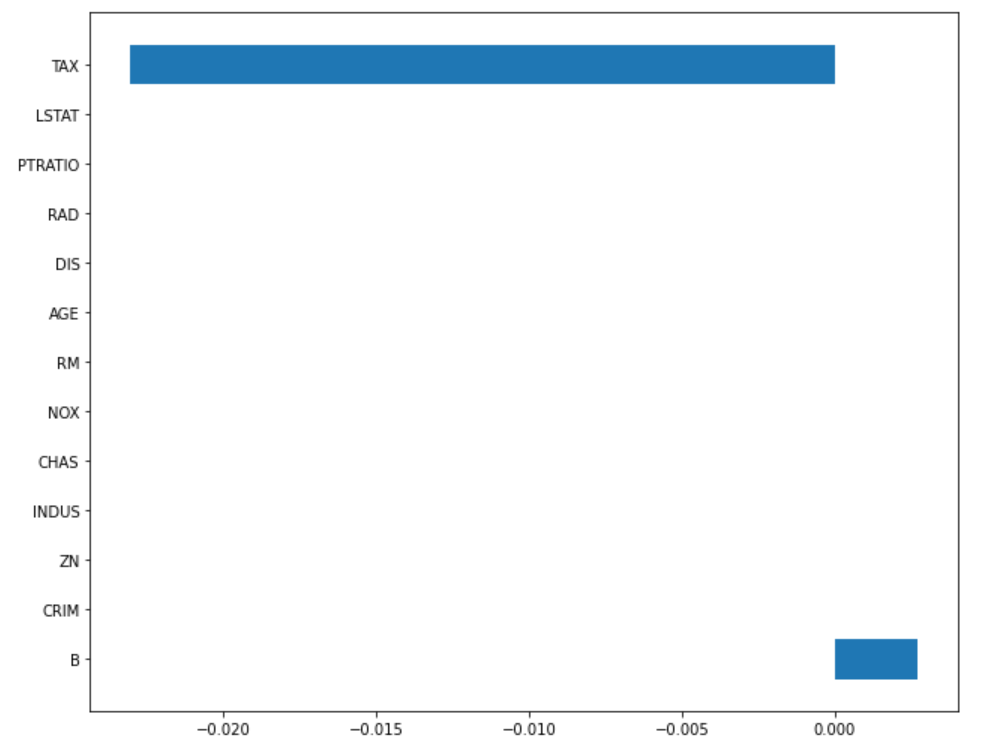

α = 0.001

plot_coef(x_train.columns, lasso_001.coef_)

엘라스틱넷(ElasticNet)

엘라스틱넷은 릿지모델과 라쏘모델을 섞은 하이브리트 형태의 모델을 말한다.

l1_ratio

- l1_ratio = 0: L2 규제만 사용

- l1_ratio = 1: L1 규제만 사용

- 0 < l1_ratio < 1: L1, L2 규제 혼합 사용

- default 값은 0.5

엘라스틱넷 모델 로드

from sklearn.linear_model import ElasticNet

ratio 값

ratios = [0.2, 0.5, 0.8]

- 값이 커질수록 규제가 커짐

엘라스틱넷 모델 구현 및 시각화

for ratio in ratios:

elasticnet = ElasticNet(alpha=0.5, l1_ratio=ratio)

elasticnet.fit(x_train, y_train)

pred = elasticnet.predict(x_test)

mse_eval('ElasticNet(l1_ratio={})'.format(ratio), pred, y_test)

이처럼 α 값에 따른 MSE 수치를 확인할 수가 있다.

엘라스틱넷 모델 가중치(coefficient) 확인

위 plot_coef() 함수를 이용해 α 값은 고정, l1_ratio 값을 다르게 했을 때 coef를 확인해 보도록 한다.

elsticnet_20 = ElasticNet(alpha=5, l1_ratio=0.2)

elsticnet_20.fit(x_train, y_train)

elasticnet_pred_20 = elsticnet_20.predict(x_test)

elsticnet_80 = ElasticNet(alpha=5, l1_ratio=0.8)

elsticnet_80.fit(x_train, y_train)

elasticnet_pred_80 = elsticnet_80.predict(x_test)

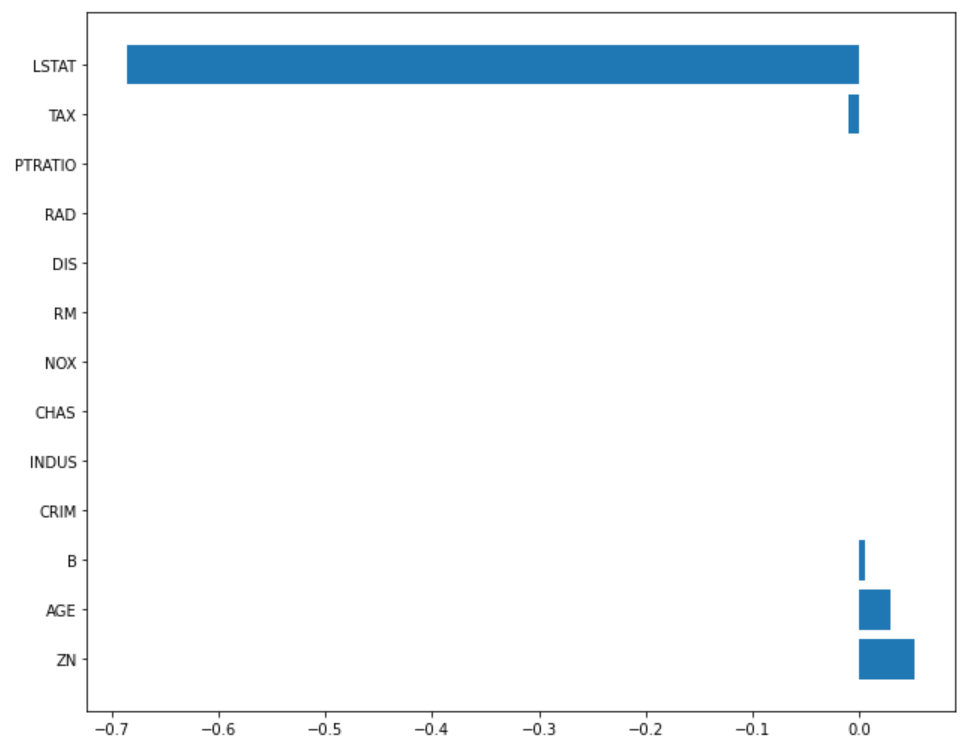

l1_ratio = 0.2

plot_coef(x_train.columns, lasso_100.coef_)

l1_ratio = 0.8

plot_coef(x_train.columns, lasso_001.coef_)

[참조] 패스트캠퍼스 - 직장인을 위한 파이썬 데이터분석 올인원 패키지 Online.

끝!